Auction Dispatch: May 2026

With over $2 bn in artworks sold in 2-weeks, lets take a data-driven look at the state of the art market in 2026.

Happy Memorial Day! I have spent my weekend pouring over the auction results from the last two weeks of sales and am excited to share what I have found.

For context, Friday concluded the marathon session of New York Art Week. Christie, Sotheby’s and Phillips auctioned off $2.3 billion in works of art across two weeks. The question hanging over the auction previews was whether the market could regain its mojo after three lean years.

Here are the highlights:

The art market recovery is real – The headline numbers confirm a rebound at the top of the market, with marquee estates and trophy works driving more than $2 billion in sales.

The recovery is barbelled – Trophy worked performed well and so did the sub $200K range. Collectors are spending aggressively at two extremes: museum-quality, historically anchored masterpieces on one end, and speculative younger artists under $200K on the other. The middle market, especially established Contemporary works priced between roughly $3M–$8M, is where hesitation, price sensitivity, and opportunity-cost anxiety now live.

Freshness, scarcity, and provenance matter more than artist name alone. The week repeatedly showed that buyers will pay extraordinary premiums for rare, fresh-to-market works with impeccable provenance, while recirculated or oversupplied material struggled even at elite price levels.

Contemporary art’s dominance is weakening as collectors rotate back toward Modern masters. Modern works outperformed Contemporary across multiple metrics, suggesting either a correction in Contemporary pricing, a broader fatigue with over-financialized living-artist markets, or a generational shift in taste toward historically validated names and canonical material.

The market has become psychologically conservative, not financially constrained. The issue is not whether collectors can spend; it is whether they feel socially and culturally validated doing so. Buyers will still chase works that feel unquestionably important or cheaply speculative, but they are increasingly unwilling to be the lone believer on expensive, fully priced material.

Deeper dives below. This is a long analysis. Fair Warning.1

State of the Market

The backdrop, on paper, was the most encouraging it had been in some time. The market recalibrated meaningfully in 2025 with auction sales increased for the first time since 2022, the share of lots selling above their low estimate rising for the first time since 2021, and sell-through rates reaching a three-year high. It finally feels like we are finding our footing post pandemic.

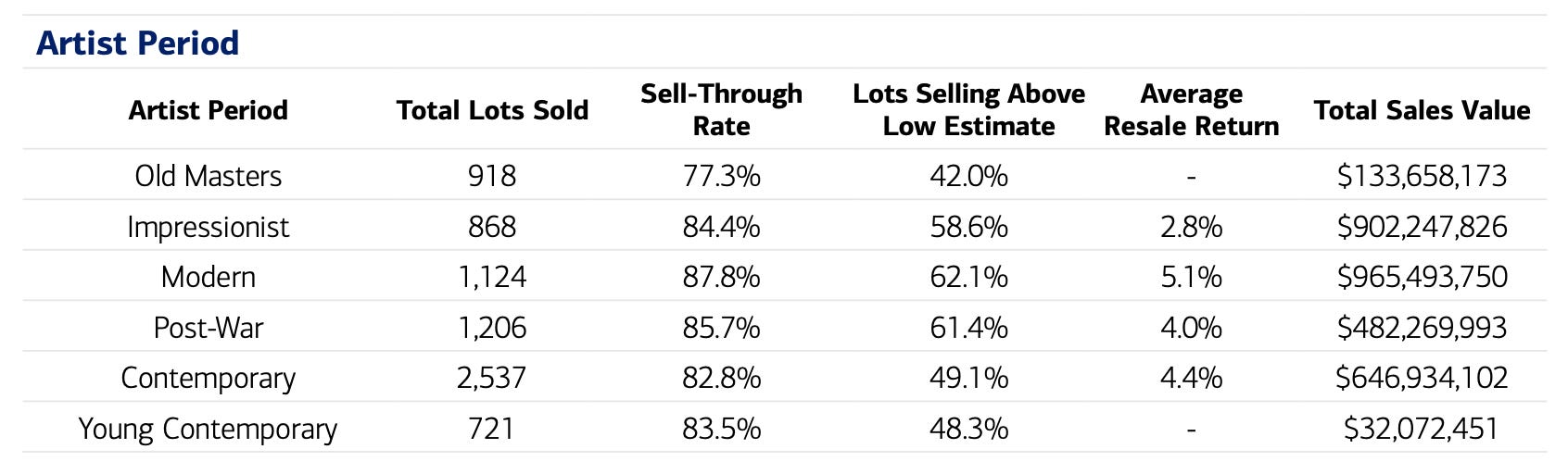

Last year we saw historical art reassert its influence while Contemporary and Young Contemporary works fell below their low estimates on average, and resale performance declined for a fourth straight year.

Advisors and market commentators have been calling this a K-shaped art market, where the most expensive works of art constitute the largest share of the sale totals. The wealth driving that top end has been compounding at roughly twice the rate of everyone else’s. A market this dependent on a thin stratum of ultra-high-net-worth buyers is, by definition, fragile to shifts in that cohort’s confidence and composition. Both are in flux right now: geopolitical shocks, increasing probability of higher top-line inflation, and the slow-motion redistribution of the Great Wealth Transfer are all reshaping who the buyer at the top of this market actually is and whether they show up.

Meanwhile, the less tested end of the auction market for young artists has retrenched, and poor auction results for living artists whose markets have been overplayed adversely affect collector confidence at the sub-$1m pricepoint. We have seen the effects of this cycle in the slew of gallery closings from the last 18 months.

Thus, the question on everyone’s mind is would the recovery story pick up the rest of the market or were we still in the middle of this correction period.

The complicating factors were geopolitical as much as economic. Middle Eastern collectors who had been active buyers faced travel constraints, European collectors were warier of coming to the United States, and an Iran conflict sat in the background of the entire week. The mood, as the dealer Marianne Boesky put it to the Times, was the variable: a lot of what has impacted the market in recent years is mood. Money was not the constraint. But that said, it rarely is.

Institutionally, the houses were betting on conviction. Sotheby’s set a low pre-sale estimate roughly 70% above its May 2025 hammer total, driven largely by Mnuchin’s Contemporary property (approximately ~33% of the Sotheby’s low-estimate) and some heavy-hitting one-off consignments (like Picasso’s Arlequin or Basiquat’s Museum Security (Broadway Meltdown); meanwhile Christie’s targeted a number between $1 billion and $1.5 billion bolstered by two big name single owner sales - S.I. Newhouse and Marian Goodman, alongside exceptional property from Aggie Gund’s estate. While the sale totals were different, the thesis remained the same. Both houses were only putting up property they were confident in, not taking risks in a market where bids feel hard won.

Now that the results are in: Around $2.3 billion of art sold across the Big Three’s (Sotheby’s, Christie’s and Phillips) evening sales, more than double last May’s equivalent.2 The recovery thesis held at the level that matters most for headlines, i.e. the very top.

But the same structural tension the BofA report identified ran straight through the week. The week was excellent at the very top and electric in the sub-$200K bracket. It was the middle that suffered. The works without exceptional provenance, the names with mature markets, the eight-figure pictures that have circulated before did not inspire the frothy bidding we saw in other parts of the market. The adviser Lorinda Ash, leaving the Christie’s salesroom, put it precisely: there is no ceiling on what people will spend, but they are just not spending money in the middle.

I’m going to reframe this K-shaped market narrative. The “K” implies a structural bifurcation where two cohorts diverge permanently. What I think I saw this week is more of a barbell.

At one end, collectors were willing to commit serious capital to top-tier, fresh-to-market, historically anchored works (the Pollock, the Brâncuși3, the Matisse). These are “low-risk” for these buyers: the works are fresh-to-market, carry irreproachable provenance, and almost nothing like them will be available again. The premium for that kind of cultural certainty is very high at the very top, and the bidding reflected it.

At the other end, the same collectors, or a different generation of them, were perfectly willing to spend on younger talent at prices where the downside is manageable. For evening sale buyers, the sub-$200K is the bracket where you buy more instinctually. The Nishimuras and the Ding Shiluns of this sale are “risky” meaning they have short auction histories and their future relevance is unknown. But the ticket price makes the risk feel like a bet, not a liability, to this collector base. That bracket ran at nearly 400% of low estimate.

What the middle proved sensitive to is opportunity cost. The $3M–$8M Richter, the established Contemporary name at full valuation, the circulated work with a known market, these are the lots where a serious collector has to ask a hard question: why this, why now, at this price? And increasingly the answer is: I’d rather take that capital and go on a shopping spree in the bottom of the market, hold it for something genuinely irreplaceable, or frankly deploy it somewhere else entirely. The middle is suffering because collectors have decided it isn’t worth the opportunity cost relative to the alternatives on either end of the room.

I. The Top Line — The Market is Back and it Looks Different than Last Time

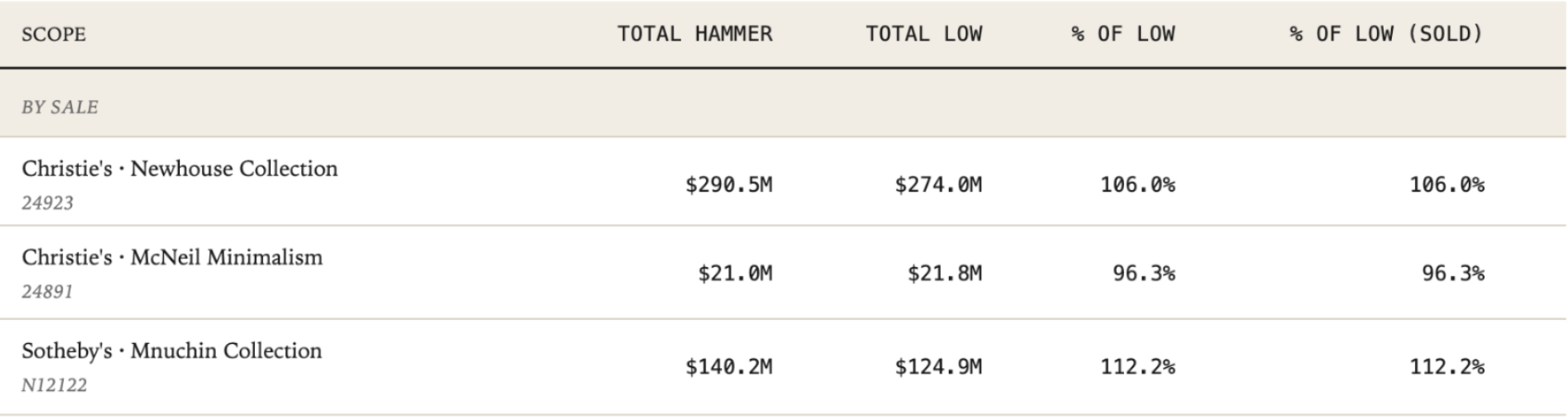

Last year, I argued that personal taste had become one of the market’s organizing principles. That tightly curated, fresh-to-market, single-owner sales were where collectors at the top level wanted to spend their money. This season, we see this pattern repeating with Newhouse and Mnuchin, but floundering with the more conceptually challenging works from The McNeil Minimalism sale.

This reads to me that collectors at this level want certainty, comprehensibility and for everyone to “ooo” and “ahh” when they say “I bought this for $10m at auction” rather than contend with the people saying “well, I could have made that I don’t get why it’s $10m.”

But before we dive in, let’s look at the scoreboard. Across the seven marquee evening sales I tracked, Christie’s hammered $749 million and Sotheby’s $534 million. That looks like roughly $1.7 billion all-in with fees across both houses.

The Single Owner Sales

The week was carried by landmark collections: the Newhouse estate at Christie’s, whose sixteen works brought $630.8 million; the white-glove Mnuchin collection at Sotheby’s; the trove of Marian Goodman Richters; Aggie Gund’s stunning Rothko etc. Two Newhouse lots cleared $100 million: the Pollock at $157 million, nearly tripling the artist’s previous record, and the Brâncuși at $93 millions. The trophy market, which contracted nearly 47% in 2024 before rebounding last fall, is definitively back.

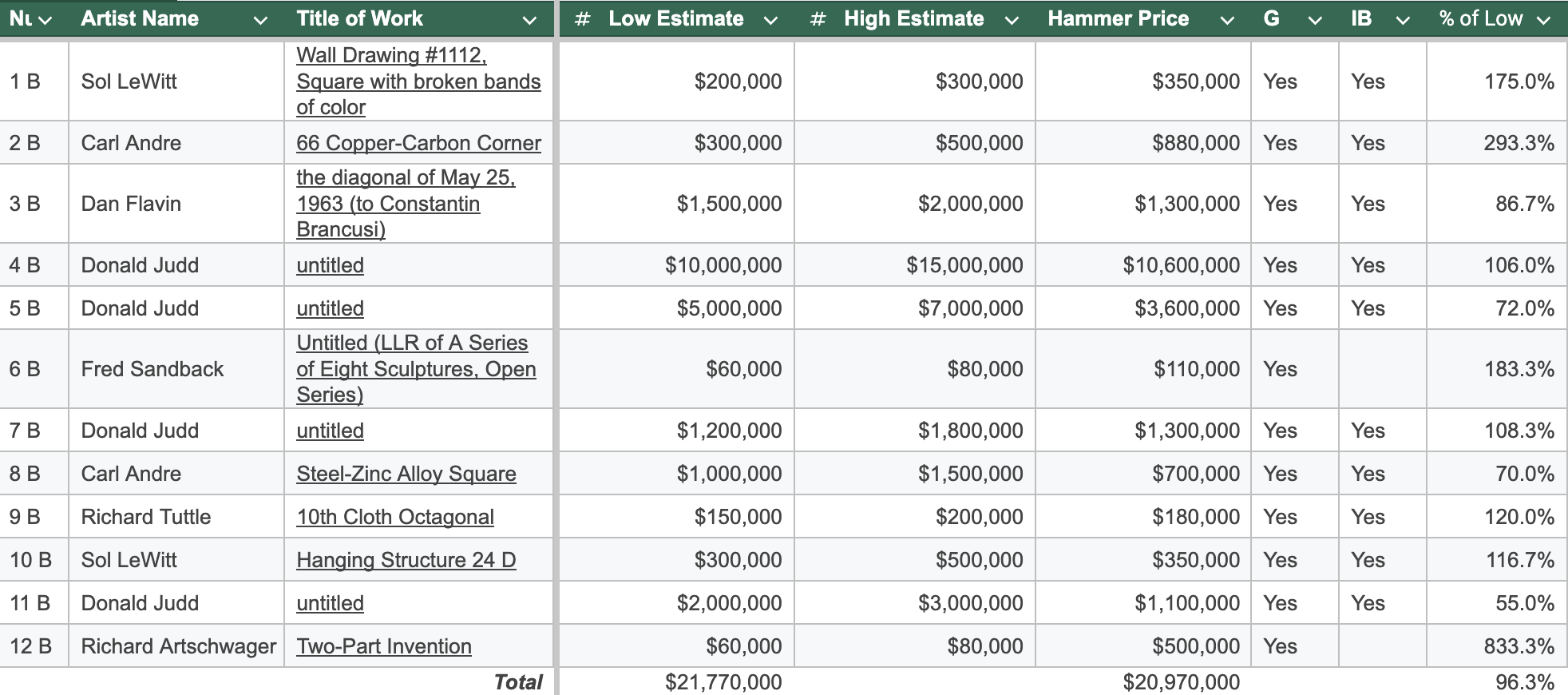

The McNeil sale is the asterisk on success for every market watcher of this week. While it was a white-glove, single-owner, four of its twelve lots hammered below their low estimates. The aggregate landed at 96.3% of low, the only sale this week that failed to clear its own floor.

Four works went under the low estimate and did not recieve that much bidding meaning they likely went to their IB’er. That being said, two outliers rescued the headline: the Judd plexiglass and copper stack drew a genuine three-way fight and set a record for the format, and a Richard Artschwager estimated at $60,000–$80,000 hammered at $500,000 after four bidders chased (833% of low estimate).

The bright spot was Modern. Sotheby’s $304 million Modern Evening sale, the night after Christie’s billion-dollar Monday, confirmed collectors are rediscovering their love for the classics of art history’s canon. Buyers were reprioritizing institutional names from the history books and prizing freshness to market and excellent provenance, both of which this season’s generational wealth transfer is bringing back to the rostrum. In addition, we are seeing more and more reports of younger collectors buying into Modern Masters. Artnet News reported one 30-something collector purchased Edgar Degas’s Femme à sa toilette (1894) for $4.3 million, below its low estimate of $5 million. Debatable if this is a bright spot but wanted to mention.

II. House by House

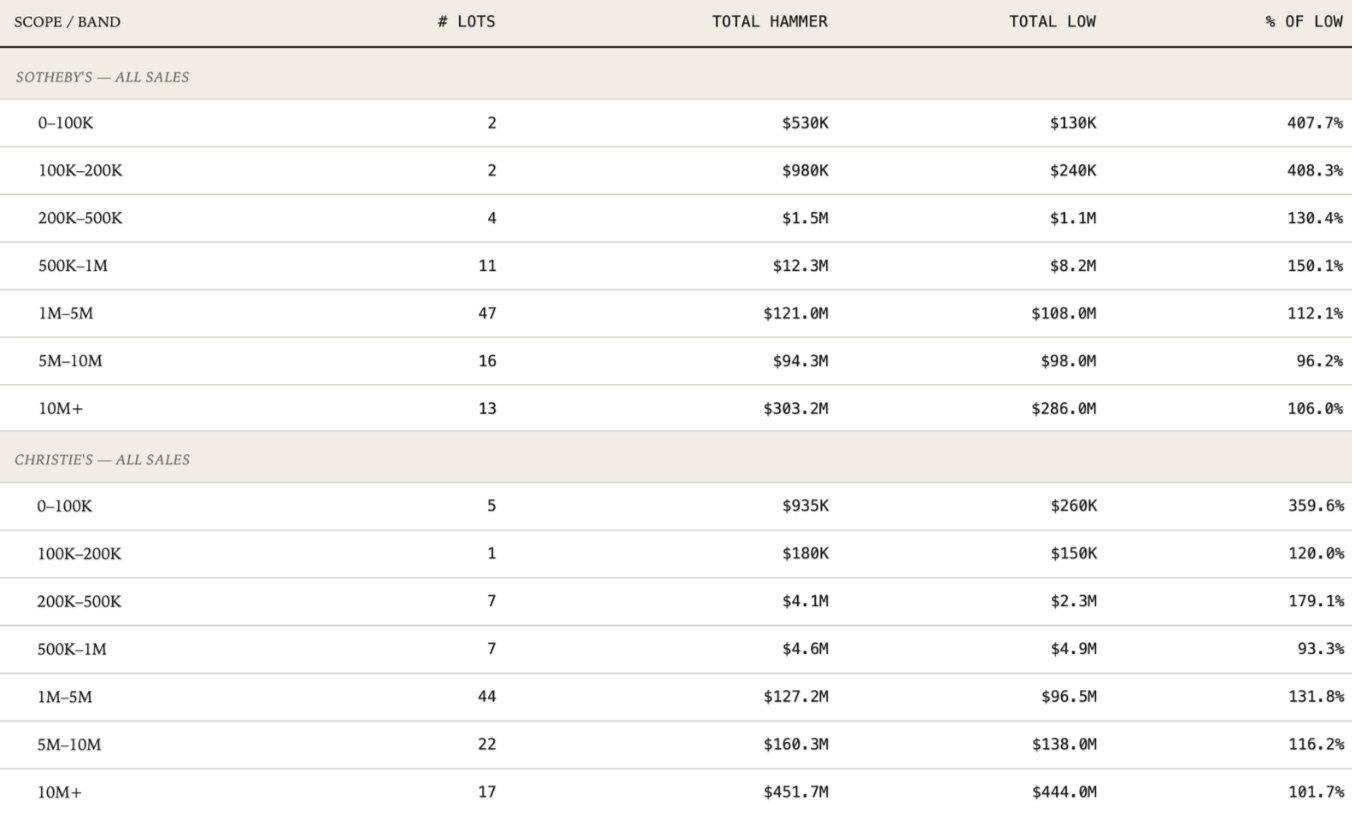

Christie’s won the week on totals: $749 million in hammer to Sotheby’s $534 million, 109.2% versus 106.4% of aggregate low estimate. But, it isn’t so clean-cut a story as “Christie’s won, and Sotheby’s lost.”

Christie’s Monday belonged to the blockbuster estates. Sotheby’s filled their sale with more conservatively estimated material that drew steady competitive bidding and it shows in the brackets below the trophy tier.

Christie’s dominated with the $1M+ bands, driving their winning headlines and incredible results with the single-owner sales. But, in the $500K–$1M band, Sotheby’s lots hammered at 150% of low across eleven works. Christie’s equivalent: 93.3% across seven works, which shows a house pricing their middle market more richly than the collectors are willing to pay.

Below $200K, Sotheby’s ran near 400% of low, driven by a small cluster of young-artist results whereas Christie’s was around 346% of the low.4

Sotheby’s also confirmed something structural about geography. The Modern Evening sale closed at a 98% sell-through, and Asian buyers stood behind its strongest moments. The top lot, Henri Matisse’s La Chaise lorraine, fresh from the Barbier-Müller collection and unseen on the market for more than a century, sold for $48.4 million to a buyer in Asia, the second-highest auction price for the artist.

Asian collectors were underbidders on the Klee, the Chagall, and one of the O’Keeffe; an Asian collector under forty took the Degas. This is the dividend of Sotheby’s Hong Kong infrastructure and year-round programming, and as we see increased institutional energy going into Asia (Frieze Seoul, Art Basel Hong Kong, Kochi Biennale, alongside satellite fairs in Southeast Asia) I’m certain we will continue to be talking about this for seasons to come.

III. The Barbelled Recovery

The week’s real structure was a barbell, and it resolves into focus across all seven sales rather than any single one.

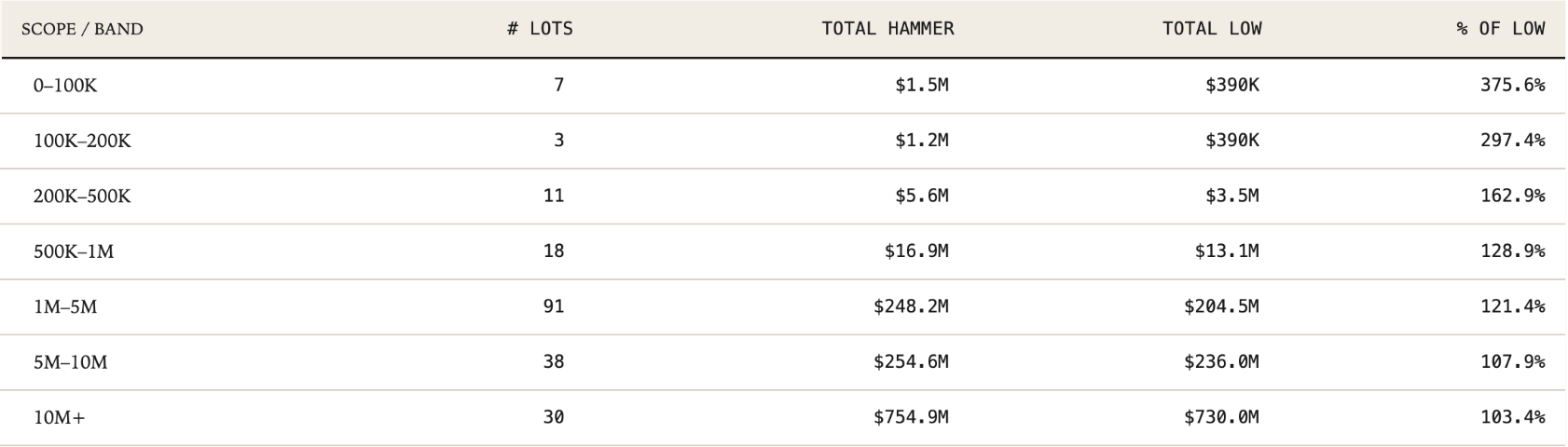

The low end outperformed. The 0–100K band hammered at roughly 375% of low; 100K–200K at nearly 300%. These were the lots with no guarantees and a lot of in-room bidding. Where there was no backstop and the price of entry was reasonable, bidders competed freely and prices ran.

The high end outperformed where the material had been off the market for over 10 years, but only there. Pollock tripled his record, Aggie Gund’s Rothko made $85 million, Matisse’s La Chaise lorraine posted the artist’s second-highest result. Each was fresh to market, scarce, and chased.

The counterexamples are what drives this home. Gerhard Richter’s Kerze (Candle), the eighth Richter of a single night and shadowed by the question of whether the market could absorb the volume, hammered at $30 million, which was 86% of low, below estimate and the weakest result of its group. Willem de Kooning’s Untitled III at Sotheby’s Contemporary Evening, estimated at $25M–$35M and carrying an irrevocable bid, came in at 88.1% of low. Two eight-figure works, both below their own floors. At the high end it is freshness and scarcity that drive outperformance, not price level. Recirculated or supply-heavy material came in soft even at the top.

The middle stayed disciplined. The $1M–$5M band reads at 121% of low in aggregate, a number flattered by guaranteed single-owner lots. Strip those out and the various-owner results in that bracket tell the harder story: established names hammering below estimate, lots clearing only because there was a guarantee. This is the bracket that demands a serious collector without offering trophy status, and it is the bracket still waiting for someone to bid first.

Modern rising, Contemporary spotty. Contemporary art has dominated the auction market for the last two to three decades and last week, we started to see some cracks. Modern lots hammered above their high estimates 37% of the time; Contemporary managed that 22% of the time and carried the highest below-low rate of any category. Is it a market correction or a shift in cultural priorities?

IV. The IB Dynamic

As a primer before we jump into this section, let’s recap what Guarantees and Irrevocable Bids are: Before the auction, the house underwrote their valuation for the collector and offered a Guarantee if they sold with the house. Then they find a third party to commit capital in the form of an IB that could match their Guarantee to ensure the work sells, and the house isn’t on the hook for the Guaranteed amount. Absent that backstop, the work may not have come to auction at all.

Alternatively, when works get an G/IB after the catalogue comes out and before the sale, the likelihood is that there was not a ton of interest at the advertised pricepoint and rather than withdrawing the lot or letting it Buy-In (not sell, signalling major market un-confidence for its advertised value) the auction house can get a G/IB set up, securing the sale for the owner.

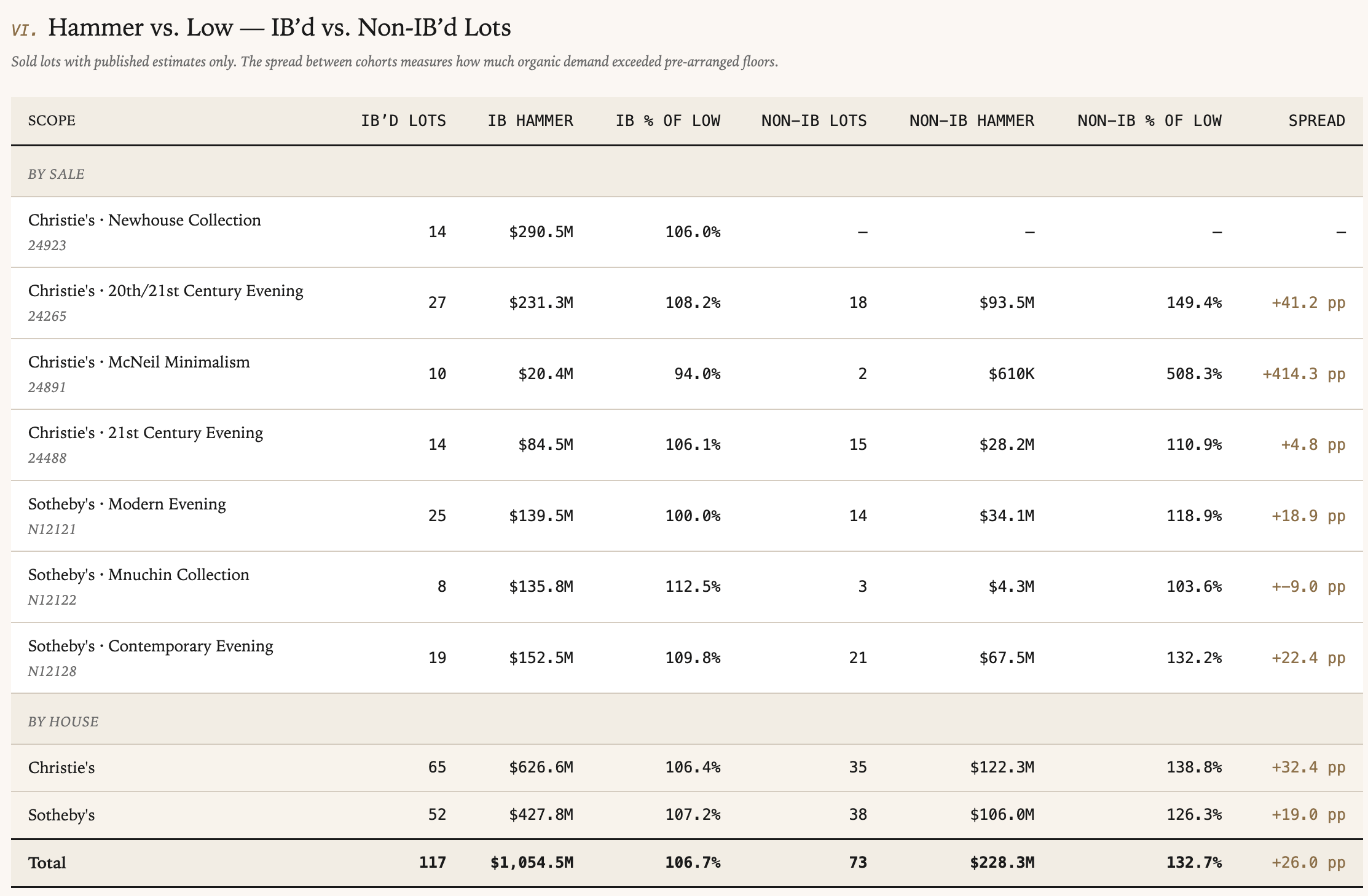

In both cases, but specifically in the latter, the irrevocable bidder is frequently the buyer, or close to it. We saw this persist this season with thirty-six IB’d lots this week hammered within 10% of their low estimate, which is to say they almost certainly went to the guarantor at one increment above the agreed floor.

There is a critique often levied at the preponderance of G/IBs on the market – that they suppress the enthusiasm of the market. What happens in reality, as with everything else at auction, is psychology as much as price mechanics. Many of these guaranteed lots require a lot of backstage work to sell. A bidder who likes a work and is willing to pay near estimate faces a choice when there aren’t other bidders around them. Depending on their personal psychology, if they can stand apart from the crowd, they lean in, convinced it is a steal. Or they need validation that what they like is desirable to others, so they don’t bid if no one else is bidding, deciding the rest of the room must know something they do not. In a salesroom full of sophisticated players drawing on the same advisors and the same research, the absence of competing bids is information. Nobody wants to be the one holding the bag at the end of the night.

With that said, lets look at the performance of the Guarantees and Irrevocable bids for the season. Lots with an irrevocable bid hammered at an average of 106.7% of low estimate, whereas lots without one hammered at 132.7% - when they sell which is an important caveat (see above). A 26-point spread, and it holds at both houses - Christie’s 106.4% versus 138.8%, Sotheby’s 107.2% versus 126.3%. Christie’s 20th Century Evening was the most extreme single case: 108.2% for IB’d lots against 149.4% for the rest, the same room, the same night.

The Brâncuși is this dynamic at its most visible. Danaïde, a 1913 bronze with provenance running back to the Meyers’ acquisition at Brâncuși’s 1914 New York debut, carried an estimate upon request near $100 million. Newhouse bought it in 2002 for $18.2 million, then a record for a sculpture at auction. On Monday it opened at $82 million and sold for a $93 million hammer a new record 51% above the artist’s previous high, and the second-most-expensive sculpture ever sold at auction. It drew a single bidder: the third-party guarantor. The most expensive sculpture of the week was, mechanically, a private transaction with an audience.

The exception that proves the rule is Mnuchin. It is the only sale this week where IB’d lots outperformed non-IB’d ones, 112.5% to 103.6%. This is a function of the deal structure. Mnuchin came in with a global guarantee, meaning Sotheby’s guaranteed the whole collection and then looked for irrevocable bidders on each lot later. What this sale result shows is that the IB’ed lots were the more attractive property, meaning the IB’ers were confident they would sell, or wanted to bid on them anyways so may as well lock that in with some potential upside if they don’t win.

V. A Richter in Two Markets

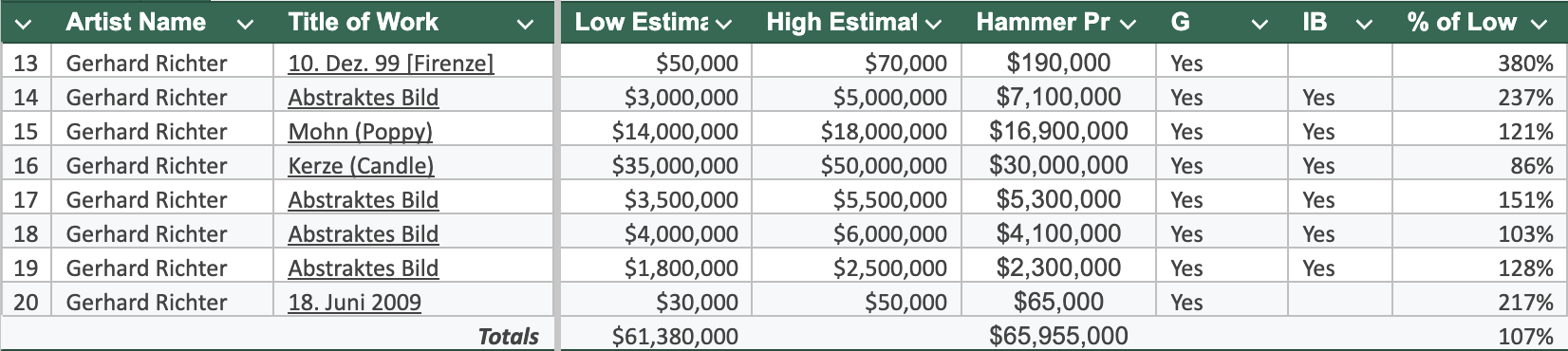

The Goodman Richters deserve their own analysis, because eight lots by one artist on one night is a level of market supply we are unused to seeing at auction.

The six major paintings, all guaranteed and IB’d, averaged 107% of low. Kerze came in below estimate at 86%. The others cleared their low estimates to mixed success. These are the $1.8M–$35M abstractions that a certain collector bought with appetite a decade ago. That collector is currently watching. As one adviser noted afterward, a dealer who had recently been willing to pay up to $5 million for a Richter abstract sat through the entire group without raising a hand.

Then the two small works on paper: an overpainted photograph estimated at $50K–$70K that hammered at $190,000, and a small 2009 work estimated at $30K–$50K that made $65,000. 380% and 217% of low, with multiple bidders. Novelty once again.

VI. Biggest Winner and Biggest Loser

Yu Nishimura, again. Last May I flagged his Across the Place going to $320,000 against a $50,000 estimate. This May, Leaves Carpet hammered at $780,000 against a low estimate of $120K. This means it achieved 650% of low and set a new record. The lot immediately before it, Ding Shilun’s Three Princes, made $280,000 against a $50K low estimate making 560% of the low estimate. There is increasing evidence now that this cohort, young, often non-Western, primary-market-backed, figurative painters, are making some consistent noise.

The biggest haircut of the week went largely unreported. The press named Eric Fischl’s The Pizza Eater (sold at 41.7% of low) as Wednesday’s steepest discount. But Christie’s Monday Evening sale produced worse: Pierre Bonnard’s Nu aux babouches rouges, estimated at $800K–$1.2M, hammered at $300,000. That is 37.5% of low, the weakest result for any sold lot all week. It is a canonical Post-Impressionist nude with a G/IB, that somebody now owns at thirty-eight cents on the dollar.

The Read-Through

At risk of repeating myself, here are the takeaways:

The trophy is back

The sub $200K range is active and exciting – keep an eye on figurative, non-western painters at this level as I believe they will continue to rise

Contemporary’s chokehold on the market is showing some cracks – time will tell if this is a pricing issue, or if the generational wealth transfer is changing collector tastes (both in what quality property is available and who has the funds to buy it)

And the truest measure of where we actually are: if you strip out Newhouse, the remaining six sales still hammered roughly $1.4 billion with fees which is about 65% above last May. That shows the art market recovery is real.

Methodology Notes

Prices are quoted in Hammer Prices unless otherwise noted

% of Low Estimate is = Hammer Price / Low Estimate

There are now more than 3K subscribers to Gnosienne and I have to say thank you! It is such a pleasure to share my passion for all things art and the art market with you and am humbled that so many people are excited to learn about it. So thank you <3

I only tracked Christie’s and Sotheby’s this year, omitting Phillips. Much of my personal interest in marquee auctions comes from the Guarantees and Irrevocable bids, which requires logging details one the catalogues go online, to see what works have come in with a deal, and checking every couple of days (sometimes hours leading up to the sales) to see where contracts are being struck on weakness leading into the sale room. I didn’t get around to logging Phillips until it was too late, will revert back next year.

We will talk about this Brancusi later in-depth

Caveat this with Christie’s offered more property at this value-band than Sotheby’s did.

Outstanding analysis thank you Georgia!